Posts Tagged ‘tax planning’

What Is a Capital Expense? A Simple Tax Guide for Business Owners

In a Nutshell A capital expense is money you spend on something that benefits your business for more than one year. Think buildings, equipment, vehicles, machinery, that kind of stuff. Unlike regular business costs (rent, salaries, paper clips), you can’t deduct the full amount the year you buy it. Instead, you spread the deduction across…

Read MoreHow Business Owners Can Keep More of Their Money in 2026

Running a business is hard. Watching a big chunk of your profit walk out the door every April is harder. If you’re earning well into the six figures, the difference between a good tax year and a great one isn’t luck. It’s planning, mostly. And maybe a little stubbornness about not overpaying. This post is…

Read MoreWhy Basic Tax Prep Is Not Enough Anymore

If you earn a high income, basic tax prep can feel like enough. You gather your documents.You send them over.Your return gets filed.You move on. That works. Sort of. The problem is that filing a tax return and planning your taxes are not the same thing. A lot of high-income earners do not realize that…

Read MoreWhy Cash Flow Planning Matters Just as Much as Tax Planning

A lot of high-income business owners spend plenty of time thinking about taxes. That makes sense. Taxes are visible. Painfully visible, sometimes. You see the payment. You see the estimate. You see the accountant’s email and think, that number cannot be right. Cash flow is different. Cash flow problems often build quietly. You can make…

Read MoreSafe Harbor Rules: How to Stay Penalty-Free Without Guessing

If you’ve ever tried to “wing it” with estimated taxes, you know the feeling. You have a strong year. Cash hits your account. You think, I’ll sort it out later. Then “later” shows up as a surprise IRS underpayment notice. Not huge. Just annoying. And it feels avoidable, because it usually is. That’s what safe…

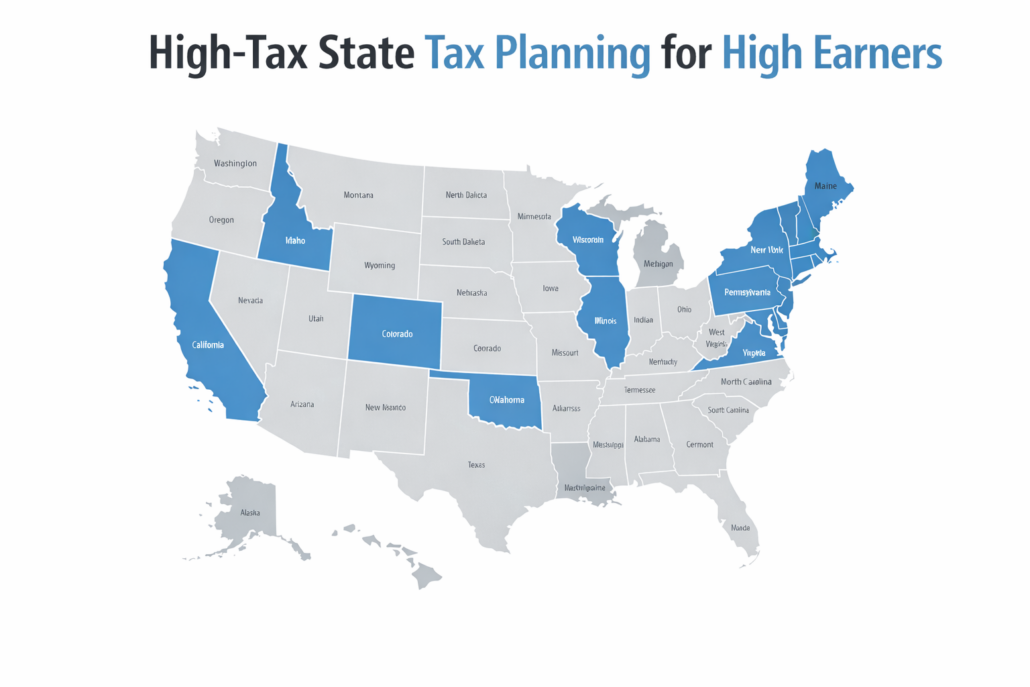

Read MoreWhich Taxpayers in High-Tax States Benefit Most?

If you live in a high-tax state, you’ve probably had this moment. You look at your paycheck.You look at your business profit.You look at your state tax bill. And you think, “Wait. Who is this even for?” High-tax states can feel like a one-way street. You earn more, you pay more, and the math starts…

Read MoreTax Planning vs Tax Preparation Fees: What’s Deductible and What Isn’t (Business + Personal Breakdown)

You pay your CPA. You get the invoice. You glance at the total and think, wait… can I write any of this off? If you’re a high earner, that question comes up a lot. Sometimes you’re paying for straight tax prep. Sometimes it’s tax planning. Sometimes it’s both mixed together, plus bookkeeping, payroll, entity cleanup,…

Read MoreAutomate Your Finances Without Losing Control: Guardrails for High Earners

Automation sounds like freedom. Bills paid. Savings handled. Taxes set aside. No scrambling. No late fees. No “where did my money go” moment at the end of the month. But if you’re a high earner, automation can also feel… risky. Because your income might swing. Your taxes might surprise you. Your “normal” month could include…

Read MoreWaiting on a Refund? You Might Be Missing Better Tax Savings Moves

You get to April, you file, and then you wait. And wait. If you’re a high-income earner in medicine, that refund can feel like a small win. A little relief. A moment where you think, I guess I did something right. But here’s the twist. A refund often means you overpaid during the year. The…

Read MoreIs Your Tax Strategy Stuck on Repeat? A Groundhog Day Wake-Up Call for High Earners

If you earn a lot and you run something on the side (or as your main thing), you probably know this feeling. You make good money. Your business grows. Your 1099 income climbs. Then tax season shows up and you think, “Why is this the same stress again?” Same scramble. Same guesswork. Same surprise bill.…

Read More