Taxes

What Counts as a Safe Harbor Tax Payment? A Beginner’s Guide for High Income Earners

In a Nutshell If you’re a high income earner, the IRS expects you to pay taxes throughout the year, not just in April. A safe harbor tax payment is basically a “get out of penalty free” card. Pay enough during the year and you won’t owe underpayment penalties, even if you end up owing a…

Read MoreBusiness Vehicle Depreciation Explained for Beginners

So you bought a nice vehicle for the business. Maybe a loaded SUV, a clean pickup, something fancier. And now your accountant is throwing words at you like MACRS, Section 179, bonus depreciation, luxury auto caps. Your eyes glaze over. Same. Here’s the thing. If you’re earning serious money, the way you handle that vehicle…

Read MoreWhat Is a Capital Expense? A Simple Tax Guide for Business Owners

In a Nutshell A capital expense is money you spend on something that benefits your business for more than one year. Think buildings, equipment, vehicles, machinery, that kind of stuff. Unlike regular business costs (rent, salaries, paper clips), you can’t deduct the full amount the year you buy it. Instead, you spread the deduction across…

Read MoreHow Business Owners Can Keep More of Their Money in 2026

Running a business is hard. Watching a big chunk of your profit walk out the door every April is harder. If you’re earning well into the six figures, the difference between a good tax year and a great one isn’t luck. It’s planning, mostly. And maybe a little stubbornness about not overpaying. This post is…

Read MoreReal Estate Investing for Doctors: Tax Benefits Beyond Depreciation

In a Nutshell; You probably already know real estate investors talk about depreciation like it’s some kind of magic spell. And sure, it is pretty great. But for doctors earning $400K, $600K, or more, depreciation alone is rarely the full story. Real estate investing for doctors: tax benefits beyond depreciation actually opens up a much…

Read MoreThe Cost of Missing Quarterly Estimated Tax Payments

Missing a quarterly estimated tax payment usually does not feel like a major problem in the moment. You may think, “I’ll catch up later.” That sounds reasonable at first. Maybe cash was tight. Maybe a client paid late. Maybe your business had a strong quarter, but the money was already tied up in payroll, debt…

Read MoreIRS Tax Relief for High-Income Earners: What Actually Works

High income does not always mean clean tax records. That sounds strange at first. You may earn more than most people. You may own a business, run a practice, receive 1099 income, collect investment income, or manage several income streams at once. Still, tax problems can show up fast. A missed estimate. A large gain…

Read MoreSafe Harbor vs. Exact Tax Payments: Which Strategy Makes More Sense?

If you earn a high income, tax time can feel strange. You can have a strong year, healthy revenue, growing accounts, and still feel blindsided when your tax bill shows up. That is where estimated tax planning gets serious. The question is not just, “How much do I owe?” It is also: “How much should…

Read MoreWhy High Earners Still Run Out of Money: Tax Mistakes, Spending Gaps, and Better Planning

You would think making a lot of money would solve the money problem. For a while, maybe it does. Then something strange happens. The income goes up, but the pressure stays. The checking account still feels tight. Taxes hit harder than expected. Big purchases start to feel normal. You save, but not in a way…

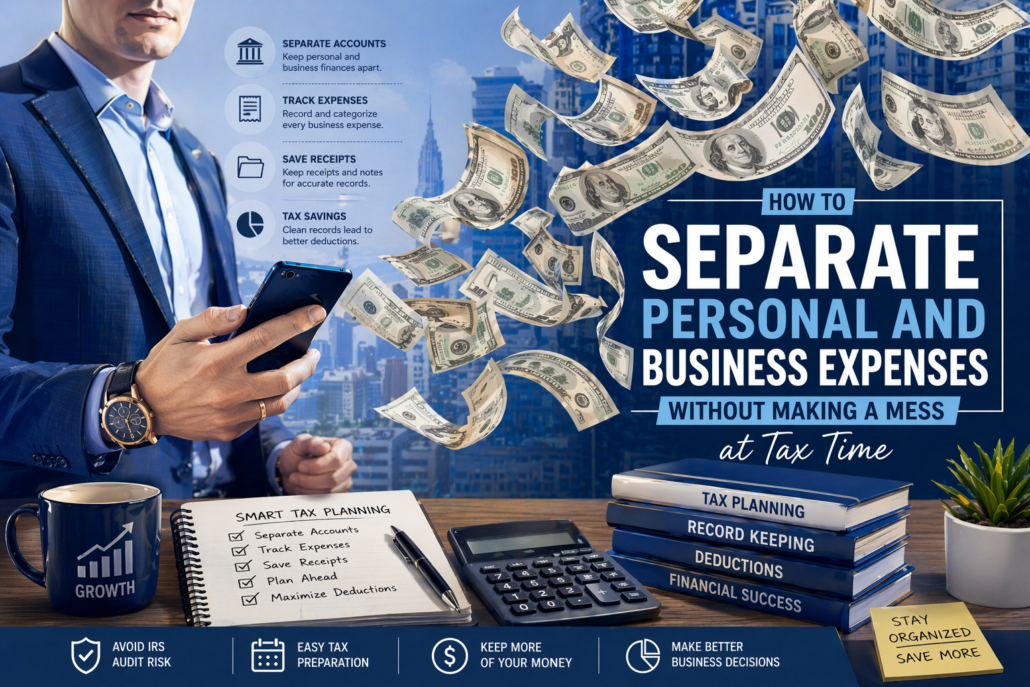

Read MoreHow to Separate Personal and Business Expenses Without Making a Mess at Tax Time

If you run a business and make good money, this issue shows up fast. At first, it seems manageable. You pay for lunch on one card. Software on another. Maybe a flight gets booked from the wrong account. Maybe your assistant grabs office supplies with a personal card and tells you later. Maybe you meant…

Read More