Taxes

Why Cash Flow Planning Matters Just as Much as Tax Planning

A lot of high-income business owners spend plenty of time thinking about taxes. That makes sense. Taxes are visible. Painfully visible, sometimes. You see the payment. You see the estimate. You see the accountant’s email and think, that number cannot be right. Cash flow is different. Cash flow problems often build quietly. You can make…

Read MoreLate K-1s and Delayed Tax Returns: What Business Owners Should Know

You’re ready to file. Your CPA is ready to file. Your numbers are mostly ready. And then one document shows up late and quietly wrecks the whole plan. That’s the K-1 problem. If you own part of a partnership, S corporation, certain trusts, or an entity invested in another pass-through business, you may need a…

Read MoreS Corp vs LLC Tax Planning: What High-Income Owners Need to Review Each Year

If you earn a lot through your business, your entity choice can quietly shape how much you keep. That sounds a little dramatic, I know. Still, it is true. A lot of high-income owners set up an LLC or elect S Corp status once, then stop reviewing it. They assume the structure still fits. Sometimes…

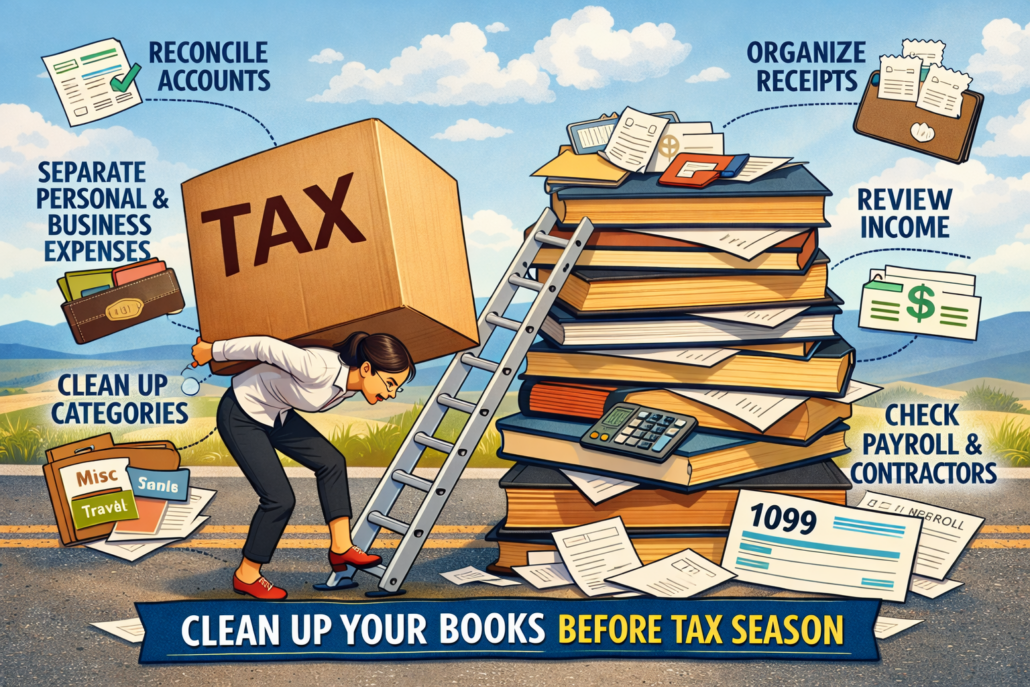

Read MoreHow to Clean Up Your Books Before Tax Season Gets Expensive

If you run a profitable business, messy books can cost you more than time. They can cost you deductions. They can create tax mistakes. They can make your return harder to prepare, which usually means more back-and-forth, more accountant time, and sometimes a bigger tax bill than you needed to have. That part catches people…

Read MoreSafe Harbor Payments: How High-Income Earners Avoid IRS Penalties

If your income is high and uneven, taxes can feel strangely easy to ignore right up until they are not. A big bonus hits. A business has a strong quarter. A K-1 shows more income than expected. You sell an asset. Suddenly your tax bill is not just bigger. It is late. And that is…

Read MoreBusiness Tax Planning Mistakes That Cost High-Income Owners the Most

If you earn a lot through your business, taxes can get expensive fast. Not just because your income is high. That part is obvious. The bigger problem is this: high-income owners often lose money through avoidable tax mistakes. Not illegal moves. Not shady things. Just missed planning. Bad timing. Poor structure. The kind of stuff…

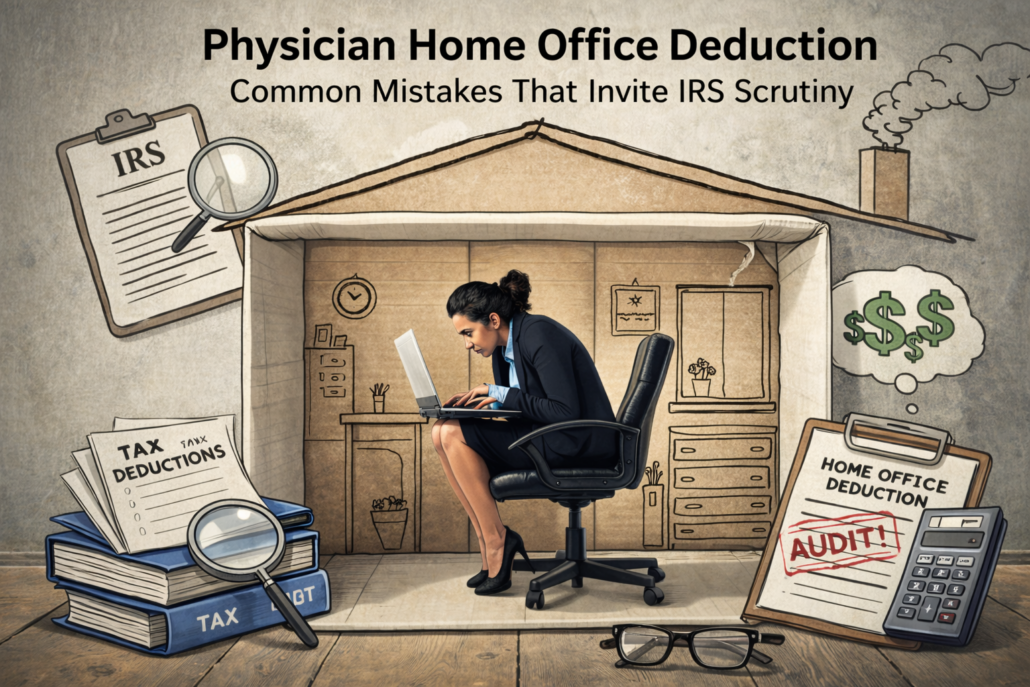

Read MorePhysician Home Office Deduction: Common Mistakes That Invite IRS Scrutiny

A lot of physicians hear the phrase home office deduction and think one of two things. Either it sounds like easy tax savings. Or it sounds like a red flag they should never touch. The truth is somewhere in the middle. The deduction is real. It can be valid. It can also get messy fast…

Read MoreWhen a Tax Advisor Can Save You More Than Tax Software

If your tax situation is simple, tax software may be enough. That’s probably the fair place to start. You plug in your numbers. You answer the prompts. You file. Done. But that starts to break down when your income gets higher, your business gets more complex, or your decisions in one area affect five others.…

Read MoreImportant March IRS Deadlines Every High-Income Business Owner Should Know

March can feel a little strange in tax season. January is loud. February is busy. March is where things get real. If you own a business, earn a high income, or have pass-through income flowing onto your personal return, this is often the month where small delays turn into penalties, late K-1s, rushed extensions, and…

Read MoreWhat to Do If You Got an IRS Notice?

You open the mail. You see “Internal Revenue Service” on the envelope. That alone is enough to ruin a perfectly normal afternoon. If you’re a high-income earner or business owner, your first thought might be that something is seriously wrong. Maybe you missed income. Maybe you triggered an audit. Maybe you owe more than expected.…

Read More